Every January, we hear the same question:

“Is it even realistic to improve my credit this year?”

And honestly, we get why people are skeptical. Credit can feel slow, confusing, and stacked against you. A lot of folks have tried before, gotten burned, or were told they just need to “wait it out.”

But here’s the truth we see at Hatch Credit: Yes. It is absolutely possible to meaningfully improve your credit in the next 6–12 months. And sometimes sooner.

Let’s talk about what that actually looks like in real life with some real examples of folks we helped last year. We’ll change names to protect privacy, but these stories are 100% real.

Real People. Real Results.

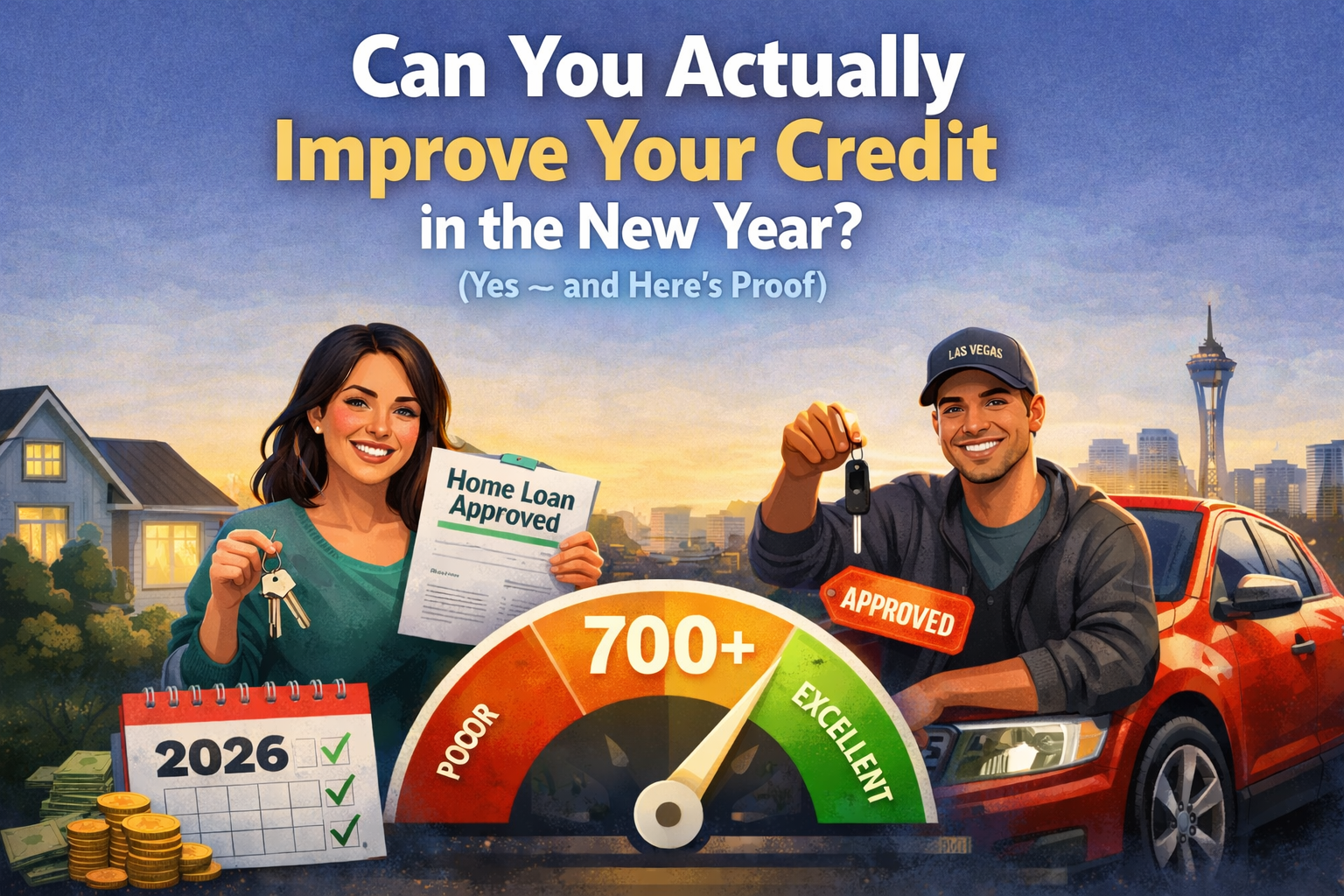

🏡 Madison’s Story (Dallas, TX)

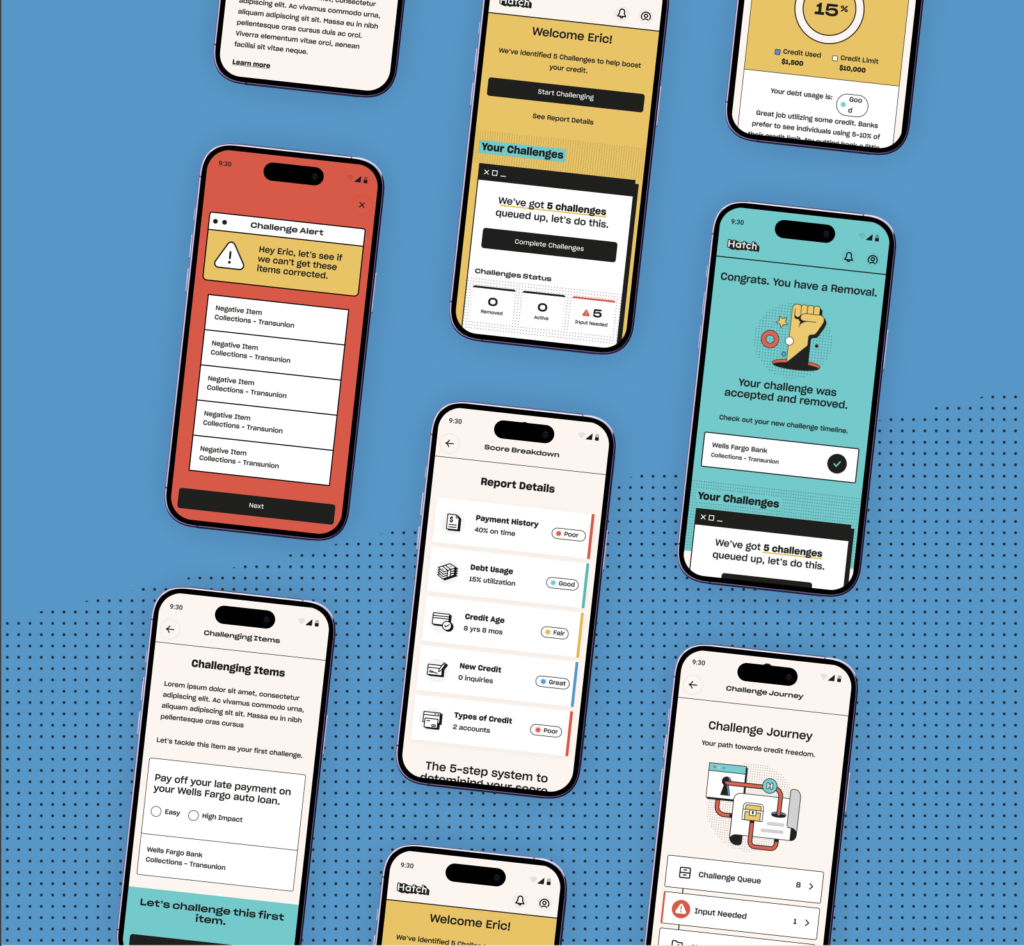

When Madison from Dallas came to Hatch Credit this past Summer, her credit score was sitting around 660. She didn’t have terrible credit, but she wasn’t getting approved for the mortgage she needed either. Madison shared she had lost her job due to COVID, fell behind on payments, and ended up with several charge-offs on her credit report. After several rounds of back and forth with her creditors and the bureaus sharing the details of her story, we were able to get those charge-offs removed.

Just a short six months after signing up, and her score is right under 790, a nearly 130 point improvement. More importantly: she got approved for her home loan and she’ll start the new year as a homeowner.

If Madison started her journey today, she’d be ready to buy a house this Summer.

🚗 Eric’s Story (Fort Lauderdale, FL)

Eric had been putting off buying a car because his credit kept getting in the way. He signed up with Hatch Credit in April and his story was a little more complicated. He shared experiences of unexpected medical bills, job loss, mistakes on his credit report, and we took it all in. Over the next several months, we shared that story with the people who needed to hear it. After the tennis match of letters back and forth we were able to help Eric raise his score by 89 points. By improving so dramatically in just seven months, Eric was able to take advantage of the year end sales and in December he drove off the lot in a new Ford F-150 with an approval he couldn’t get back in April.

If Eric started today, he could be taking the new car out for a road trip by this Summer.

Here’s the Part Most People Don’t Realize

Credit improvement doesn’t have to be a multi-year journey.

For many Hatch Credit customers, their credit improvement chapter with us lasts about 6 to 9 months.

After that? A lot of people graduate from our services and move on with their lives — with better credit and more options.

But Let’s Be Honest: Your Timeline Is Yours

Credit is personal. Each journey is very unique and can depend on a number of factors.

What is your end goal, are you looking to use your credit for a house? Car? To start a business?

What types of items are on your reports and how old are they?

What was going on in your life when those payments were missed? Were they impacted by job loss, divorce, medical emergencies, or something else?

Some people move faster. Some take a little longer. Improvement is normal. Progress is common. And success stories are not rare here.

Thinking About 2026? The Time to Start Is Now.

If your goal is to:

- Buy a house in 2026

- Get a better car loan

- Start a business

- Refinance something expensive

- Or just stop getting denied

Then here’s the simple truth, starting today gives you plenty of runway to get there. These are two real examples of customers we helped in around six months, but those timelines aren’t anomalies, we help lots of customers achieve their credit goals in under a year.

If you have goals this year, let us help you get there, get started today for just $1.